How Bangla QR is Shaping the Future of Fintech

Walk into any local grocery store, tea stall, or retail outlet in Dhaka today, and you will witness a fascinating financial transition. The familiar rustle of paper Taka notes is slowly being accompanied by the rhythmic chiming of smartphone notification alerts. Digital payments have arrived in Bangladesh, and at the absolute center of this retail evolution is a unassuming, pixelated square: Bangla QR.

For years, developing economies have chased the holy grail of a “cash-lite” society. Cash is expensive to print, risky to carry, and incredibly difficult for central banks to track. Yet, moving an entire population away from cash requires an alternative that is just as fast, universally accepted, and practically free.

To achieve this, Bangladesh Bank introduced Bangla QR—a unified quick-response code standard designed to overhaul retail commerce. But as citizens scan these codes daily, a natural point of comparison arises: India’s globally acclaimed Unified Payments Interface (UPI). How does Bangladesh’s homegrown system stack up against the gold standard of digital finance? Why does a system built for real-time speed sometimes feel sluggish? And most importantly, is this technology truly the future of finance?

UPI vs. Bangla QR

To understand where Bangladesh’s financial ecosystem is heading, we must first understand what Bangla QR actually is—and what it isn’t. It is incredibly common to hear people compare Bangla QR directly to India’s UPI, but this is structurally an apples-to-oranges comparison.

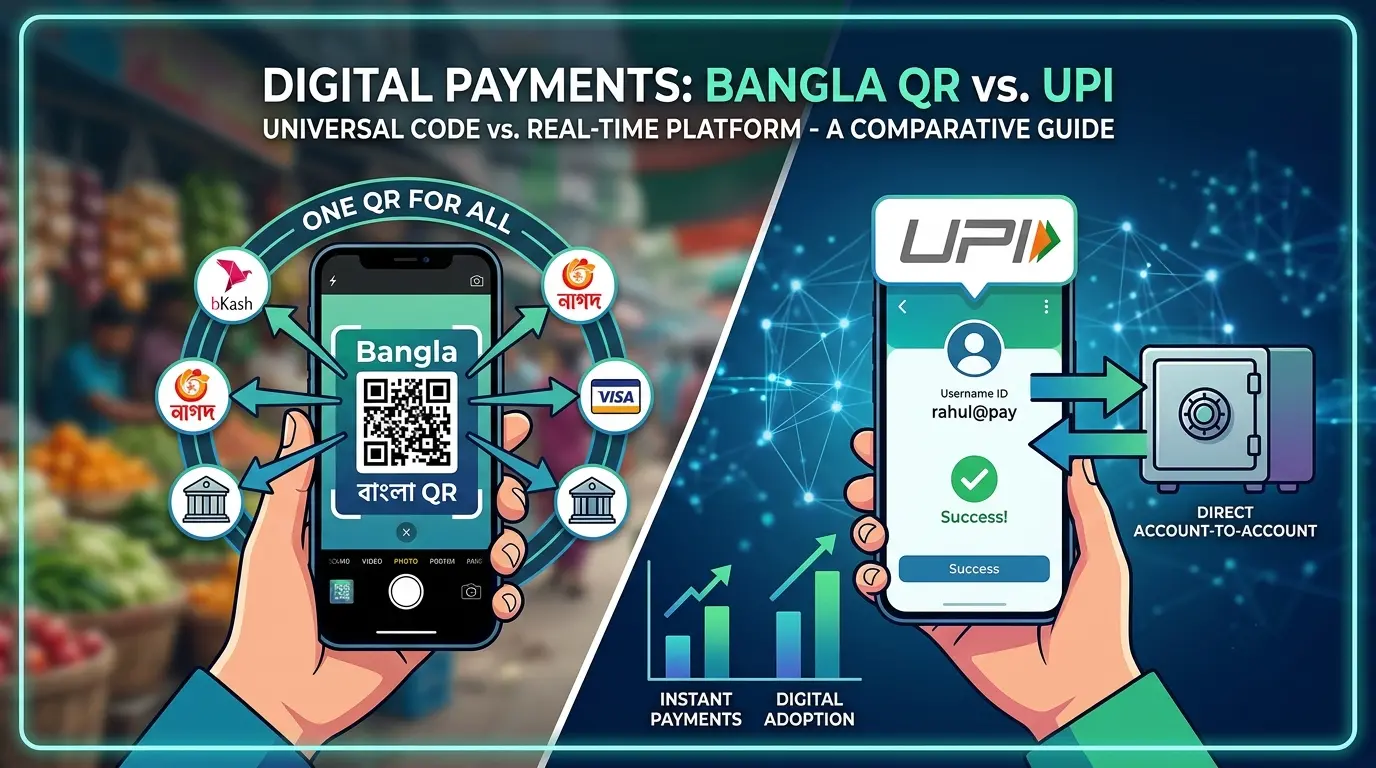

UPI: The Ultimate Financial Highway

India’s UPI, managed by the National Payments Corporation of India (NPCI), is a comprehensive, real-time banking protocol. Think of it as a massive, state-of-the-art superhighway. It bypasses traditional debit card networks entirely. Instead, it assigns every citizen a Virtual Payment Address (VPA), like name@bank. When you scan a UPI QR code, money moves directly from your bank account to the merchant’s bank account in milliseconds, completely bypassing the need for an intermediary digital wallet.

Bangla QR: The Universal Steering Wheel

Bangla QR, on the other hand, is not a backend payment network. Instead, it is a frontend universal standard.

Before its inception, the Bangladeshi retail landscape was fragmented. If a merchant wanted to accept digital payments, their counter would be cluttered with half a dozen different plastic stands: one for bKash, one for Nagad, one for Rocket, and perhaps a couple more for specific commercial banks. A customer with a bKash app could not scan a Nagad QR code. It was a closed-loop nightmare.

Bangla QR solved this by acting as a universal translator. It took all these separate, competing engines—Mobile Financial Services (MFS) and traditional banks—and forced them to speak the same visual language. Today, a merchant needs only one Bangla QR code sticker on the wall. A customer can open their bKash app, their Nagad app, or their tech-forward commercial bank app, scan that single code, and the payment will route successfully.

The Speed Paradox: Real-Time, Yet Sometimes Slow

As more users adopt Bangla QR, a common frustration has emerged among consumers and merchants alike: If this system is advertised as instantaneous, why does it sometimes feel so slow?

To answer this, we have to look at what happens behind the screen during the three to five seconds your phone spends loading.

[Your Banking/MFS App]

│

▼ (Scan Bangla QR)

[Interoperable Gateway / NPSB]

│

├─────────────────────────┐

▼ ▼

[Your Bank/Wallet] [Merchant's Bank/Wallet]

(Authorize Funds) (Receive Settlement)

When you use a closed-loop system—for example, using a bKash app to pay at a bKash-specific merchant QR—the transaction never leaves bKash’s private servers. The handshake is internal, meaning the transaction clears in a fraction of a second.

However, when you use a interoperable Bangla QR, the journey is much more complex:

- The Cross-Network Hop: If you scan a merchant’s Bangla QR using a commercial bank app, the transaction must leave your bank’s network, pass through a national clearing house like the National Payment Switch Bangladesh (NPSB), and then knock on the door of the merchant’s financial provider.

- The Banking App Bottleneck: Traditional commercial banks run on legacy core banking software. These systems were engineered for deep security and large-scale wire transfers, not for processing micro-transactions at a crowded city intersection. The time it takes for a bank’s app to log you in, check your balance, ping the central clearing switch, and verify the merchant’s credentials naturally adds a few seconds of latency.

- Network Infrastructure: In a densely populated market, mobile data speeds can fluctuate. Because an interoperable transaction requires a multi-party digital handshake, a slight drop in network connectivity can cause the app to spin endlessly, or worse, time out mid-transaction.

Therefore, while Bangla QR is technically a real-time settlement system—meaning the merchant legally receives ownership of the funds instantly—the user experience can occasionally feel sluggish compared to throwing down a physical cash note or tapping a closed-loop wallet.

Why Interoperability is the Ultimate Game Changer

Despite these growing pains, the structural shift toward an interoperable Bangla QR is non-negotiable for the future of the economy.

For the average consumer, the benefit is pure convenience. You no longer need to maintain balances across four different digital wallets just to ensure you can pay at different shops. Your money can sit safely in your primary bank account or preferred wallet, ready to be deployed anywhere.

For the macroeconomy, the implications are even more profound. Micro-merchants—the street-side tea vendors, the vegetable sellers, the rickshaw pullers—have historically been entirely cut off from the formal banking sector. They operate strictly in cash, which means they have no recorded economic footprint.

When a small business owner adopts Bangla QR, every single 20-Taka cup of tea sold leaves a digital footprint. Over six months, this transaction history creates a verifiable ledger of revenue. Suddenly, a traditional bank has the data it needs to offer that micro-merchant a small business loan, bringing millions of unbanked citizens into the formal financial fold.

The Path to a Cashless Bangladesh

Where do we go from here? The ultimate destination for Bangladesh is clear: an ecosystem that combines the universal front-end interface of Bangla QR with the frictionless, lightning-fast backend infrastructure of the UPI model.

To make this a reality, Bangladesh Bank has been aggressively modernizing its national payment gateways. The infrastructure is steadily shifting from handling purely merchant transactions (Person-to-Merchant) to enabling frictionless peer-to-peer (Person-to-Person) transfers. Imagine a future where you don’t exchange phone numbers or type in clunky 13-digit account numbers to pay back a friend; you simply show them your personal, encrypted Bangla QR code generated on your phone, and the transfer happens instantly across different platforms.

Furthermore, the cost of transactions must continue to drop. For mass adoption to mirror the success seen in regional neighbors, the transaction fees for small-scale merchants must remain at absolute zero. When digital payments become genuinely cheaper, safer, and more convenient than handling physical cash, cash will naturally lose its crown.

Bangla QR may currently experience the occasional digital stutter or a few seconds of loading latency, but these are simply the necessary growing pains of a nation rewriting its financial infrastructure. The pixelated square on the shop counter is no longer just a high-tech novelty—it is the cornerstone of Bangladesh’s economic future.