How to Invest Properly: A Beginner’s Guide to Building Wealth the Right Way

Hey there. If you’re reading this, I’m guessing you’re tired. You’re tired of scraping by at the end of the month, tired of seeing the price of groceries go up while your paycheck stays the same, and tired of the anxiety that comes with wondering if you’ll ever actually “get ahead.”

I have been exactly where you are.

Let me be clear right out of the gate: Investing does not belong to the guys in the fancy suits on Wall Street. It isn’t a secret club, and it isn’t magic. It is a tool—arguably the only tool—that the average person has to build genuine financial security. But here is the catch: You have to do it right.

If you are looking for a “get rich quick” scheme, please stop reading now. This guide isn’t for you. But if you want a boring, reliable, and proven strategy to build wealth over the next 10, 20, or 30 years, you have come to the right place. Drawing from my own painful mistakes and the timeless principles of financial history, we are going to break down exactly how to make your money work for you.

The “Why”: Why Saving Alone is a Losing Battle

You might be thinking, “Why can’t I just save money in my bank account?”

Here is the hard truth: Cash is a terrible investment.

It sounds counterintuitive, right? But we live in an economy driven by inflation. Think about what a cup of coffee cost five years ago versus today. Or rent. Or gas. Every year, the purchasing power of a single dollar drops. If your money is sitting in a standard savings account earning 0.01% interest while inflation is running at 3% or 4%, you aren’t standing still—you are actively losing money.

Investing is the shield against inflation. It allows your money to grow at a rate that (historically) outpaces the rising cost of living. It harnesses the power of Compound Interest—what Einstein reportedly called the “eighth wonder of the world.”

- Simple Interest: You earn money on your principal.

- Compound Interest: You earn money on your principal plus the money your principal has already earned.

It’s a snowball effect. But it only works if you start.

My Personal Wake-Up Call: How I Lost Half My Savings

I want to share a story that is a bit embarrassing, but necessary.

Back in my early 20s, I was desperate to escape my dead-end job. I had managed to save up a few thousand dollars—money that took me forever to scrape together. I went online and saw everyone talking about a specific tech stock (this was years ago, but think of it like the recent AI or Crypto crazes).

I didn’t look at the company’s profits. I didn’t look at their debt. I just saw a line on a chart going up and people on Reddit screaming “To the Moon!”

I felt like a genius. I bought in. For three days, I watched the number go up. I was mentally spending the profits. I thought I had cracked the code.

Then, reality hit. A regulatory report came out, the company’s hype bubble burst, and the stock plummeted. I panicked. I watched my savings get cut in half in 48 hours. Sick to my stomach, I sold everything at a massive loss, convinced that “investing is a scam.”

I was wrong. Investing wasn’t a scam. I wasn’t investing. I was gambling.

There is a massive difference between the two, and understanding that difference is the most important thing you will learn today.

The Golden Rule: Investing vs. Speculating

If you take nothing else away from this guide, take this. You need to know if you are an investor or a speculator.

1. The Speculator (The Gambler)

Speculators are looking for a quick win. They buy assets because they think the price will go up tomorrow.

- Focus: Short-term price changes.

- Strategy: Chasing hype, news, and “hot tips.”

- Risk: Extremely high. You can lose 100% of your money.

- Examples: Day trading, meme stocks, obscure cryptocurrencies, flipping options.

2. The Investor (The Builder)

Investors are looking to own a piece of a successful business or asset class over a long period.

- Focus: Long-term value and cash flow.

- Strategy: Buying quality assets and holding them for years.

- Risk: Managed. The market fluctuates, but history shows an upward trend over decades.

- Examples: Index funds, blue-chip dividend stocks, real estate.

Successful wealth building is boring. It’s not checking your phone every five minutes. It’s setting a plan and living your life while your money works in the background.

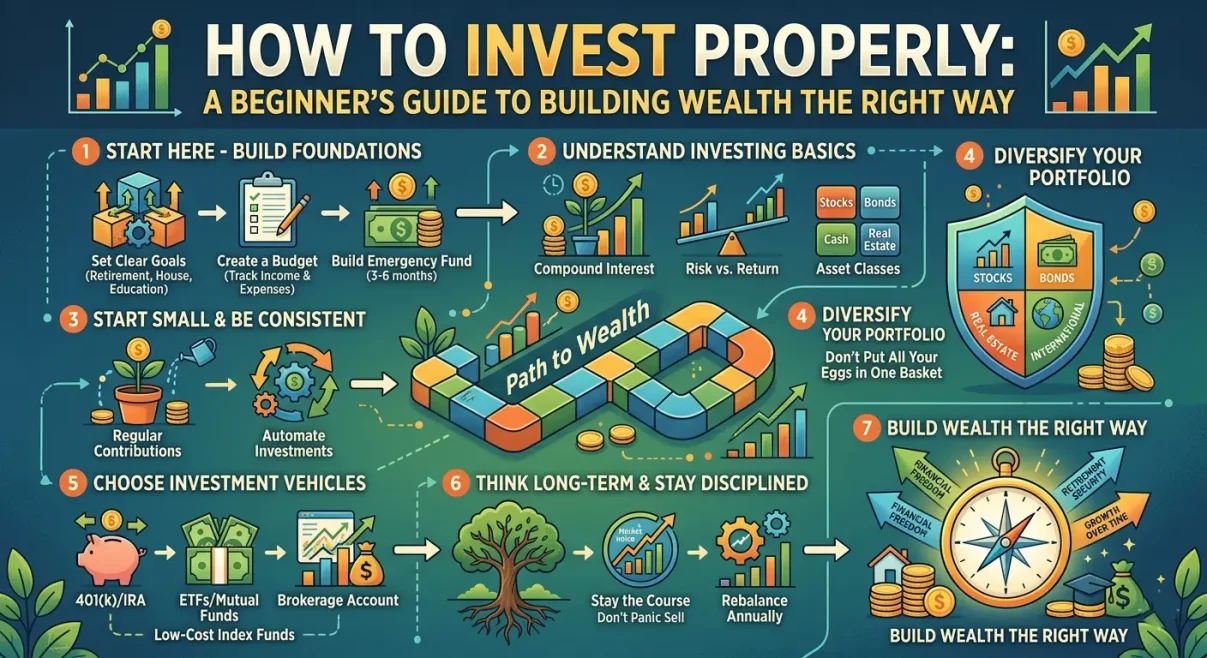

The Strategy: A Step-by-Step Guide to Doing It Right

Okay, enough theory. How do you actually do this? If I were starting over today with $0, this is exactly what I would do.

Step 1: The Vehicle (Index Funds and ETFs)

Don’t try to pick individual stocks. Even professional fund managers who get paid millions struggle to beat the market consistently. Instead of trying to find the “needle in the haystack,” just buy the haystack.

This is called an Index Fund (or an ETF).

For example, an S&P 500 ETF buys tiny pieces of the 500 largest companies in America (Apple, Microsoft, Amazon, etc.).

- Why it works: If one company goes bankrupt, you have 499 others to back you up.

- The returns: Historically, the S&P 500 has returned about 10% per year on average (before inflation).

- The tickers: Look for low-fee funds like VOO (Vanguard S&P 500) or VTI (Total Stock Market).

Step 2: The Method (Dollar-Cost Averaging)

Do not try to “time the market.” You will fail. You will buy at the top and sell at the bottom because of human psychology.

Instead, use Dollar-Cost Averaging (DCA). This simply means investing the same amount of money on the same schedule, regardless of the stock price.

- Market is down? Great, your $200 buys more shares (on sale!).

- Market is up? Your portfolio value is growing.

Action Item: Set up an automatic transfer of $100 (or whatever you can afford) every payday into your investment account. Treat it like a bill that must be paid.

Step 3: Asset Allocation (Don’t Put All Your Eggs in One Basket)

While stocks are the engine of growth, they can be volatile. A proper portfolio balances risk.

- Equities (Stocks): For growth.

- Bonds: For stability and income. (Government or Corporate debt).

- Real Estate (REITs): Funds like VNQ allow you to own real estate without being a landlord.

A simple rule of thumb-

If you are young (20s/30s), you can afford to be aggressive (e.g., 80% stocks / 20% bonds). As you get older, you shift more toward bonds to protect what you’ve built.

The Math: Why Patience is Your Superpower

Let’s look at the numbers. This is where the magic happens. Let’s assume a conservative 8% annual return.

| Monthly Investment | Time Period | Total Contributions | Total Value (approx.) |

| $200 | 10 Years | $24,000 | $36,000 |

| $200 | 20 Years | $48,000 | $118,000 |

| $200 | 30 Years | $72,000 | $298,000 |

| $500 | 30 Years | $180,000 | $745,000 |

Look at that last row. You put in $180k over a lifetime, but you walk away with nearly three-quarters of a million dollars. That is “free money” generated by the market. But notice: the big growth happens in the later years. You have to stay in the game.

Common Pitfalls (How to Not Screw This Up)

Even with a plan, your brain will try to sabotage you. Here are the traps to avoid-

- Panic Selling: When the news says “The Market is Crashing,” your instinct will be to sell. Don’t. That is the moment to buy. History shows the market has recovered from every single crash (2008, 2020, etc.).

- Lifestyle Creep: When you get a raise, don’t buy a better car. Increase your automatic investment.

- The “Fun” Money Trap: If you really want to buy crypto or pick individual stocks, limit it to 5% of your portfolio. Consider it “entertainment money.” If you lose it, your financial future shouldn’t be at risk.

- High Fees: Stick to Vanguard, Fidelity, or Schwab. avoid funds with “Expense Ratios” over 0.5%. The funds I mentioned earlier (like VOO) charge around 0.03%.

Final Thoughts: Just Start

The hardest part of investing is the first step. It feels scary to click “Buy” for the first time. But doing nothing is the biggest risk of all.

You don’t need thousands of dollars. You can open a brokerage account today with $50. You can buy a fractional share of an index fund.

- Set a goal (Retirement? A house? Freedom?).

- Open the account (Roth IRA is great for tax benefits).

- Automate it.

- Go live your life.

Years from now, your future self is going to look back at this moment and say, “Thank you.”

If you are hungry for more details on wealth strategies, finding the right brokerage, or diving deeper into market history, reputable resources like inenus.com offer excellent insights to keep your education going.

Investing isn’t about getting rich tomorrow. It’s about ensuring you never have to worry about being poor in the future. Let’s get to work.